Inward processing

When non-Union goods are subject, in the customs territory of the European Union (EU), to intervention beyond simple handling, the intervention may be carried out under the inward processing customs procedure. This concerns operations for processing, assembling, working or repairing.

The use of inward processing suspends duties and taxes due on importation.

At the end of inward processing, the processed goods may be:

- exported outside the EU

- released for free circulation in the EU

- placed in another customs procedure.

To use the inward processing procedure, operators have to apply for an authorization from the Customs and Excise Administration and provide a guarantee covering the amount of customs duties that would be payable should the processed goods be released for free circulation.

The authorization is issued by the Customs and Excise Administration for a maximum duration of five years. For goods that are covered by a European regulation, the maximum period of validity of the authorization has been limited to three years.

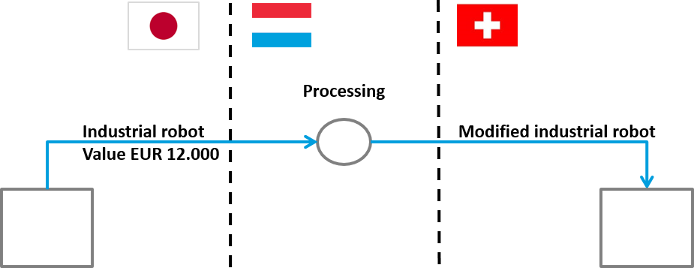

For example: a Luxembourg company is specialized in the sale of industrial robots modified for the needs of its customers. It buys the robots in Japan and then, after processing, sells them to a Swiss company.

If the company does not use the inward processing procedure, it has to pay the import customs duties at the time of the arrival of the robots in Luxembourg.

The inward processing procedure allows the company to avoid paying import customs duties on the robots that will be sold on exportation.

For a robot corresponding to Combined Nomenclature 8515 31 00 (import customs duties of 2.7%), the use of the inward processing procedure represents a saving of €324 per robot for the Luxembourg company (12,000*2.7%).

Furthermore, under certain circumstances, movement of goods placed under inward processing, may take place between different places in the customs territory of the Union without customs formalities.

Outward processing

When Union goods are subject to processing or repair outside of the customs territory of the EU, the goods may be exported using the outward processing procedure.

The goods are declared for temporary exportation and, on their return, are declared for re-importation. At the time of their re-importation, the import customs duties only apply on the added value due to the processing outside of the EU and not on the total value of the re-imported goods.

To use the outward processing procedure, operators have to apply for an authorization from the Customs and Excise Administration.

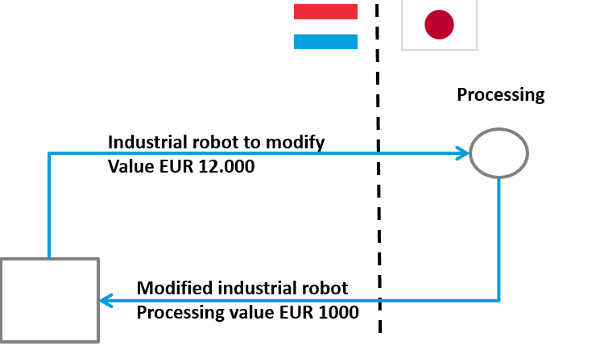

For example: a Luxembourg company is owner of an industrial robot manufactured in Japan. It sends the robot to Japan to have it processed by a manufacturer before being able to use it again in Luxembourg.

If the company does not use the outward processing procedure, it will pay the import customs duties at the time when the robot is returned to Luxembourg on its total value, i.e. on €13,000 (robot value + service value).

Using the outward processing procedure, the company will pay import customs duties only on the value of the processing, i.e. on €1,000.

For a robot corresponding to Combined Nomenclature 8515 31 00 (import customs duties of 2.7%), the use of the outward processing procedure represents a saving of €324 for the processing operation (12,000*2.7%).