Value-added tax (VAT) covers all stages of production and distribution of goods and services carried out in Member States of the European Union (EU)*.

When goods are supplied within the Member State in which they were produced, purchased, stored or imported, the seller is completing a national transaction. The supply is subject to VAT of the concerned Member State according to its applicable laws and regulations.

When goods are dispatched or transported to another Member State, the supplier is conducting an intra- Community supply. The VAT treatment of this supply depends on the status of the purchaser: taxable person or "non-taxable" person.

Intra-Community supply of goods to a taxable person

An intra-Community supply of goods to a taxable person may be VAT-exempt when the following conditions are met:

- the goods are transported outside the territory of the Member State, in which the goods are located at the time when the dispatch or transport starts

- the purchaser provides its VAT number delivered by another Member State than the one from which the goods are dispatched or transported.

In such circumstances, the supplier must:

- obtain and check the validity of the VAT number provided by the purchaser on the website of the European Commission, prior to delivery

- indicate the VAT number of its customer on its sales invoice as well as a mention of the exemption

- keep the proof of the transport of the goods outside the territory of Luxembourg. Article 45bis of Regulation 282/2011 specifies the types of proof to keep. The choice of the Incoterm is important: the use of the EX WORKS Incoterm should be avoided, because it creates a risk for the seller who is not in charge of transport.

The supplier must declare the exempt intra-Community supply of goods in its VAT return and in a recapitulative statement in the Member State from which the goods are dispatched or transported.

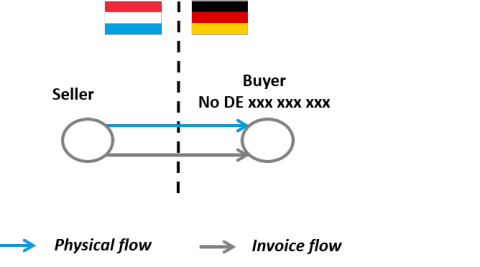

For example: a Luxembourg company receives an order from a German company that provides it with its German VAT number. It delivers the goods from Luxembourg to Germany.

The intra-Community supply to the German customer is VAT-exempt in Luxembourg.

The VAT-taxable purchaser must declare an intra-Community acquisition in the country of arrival of the transport. The declaration is made using the reverse charge mechanism: the purchaser declares the VAT due on its purchase in its VAT return and claims the deduction of VAT at the same time.

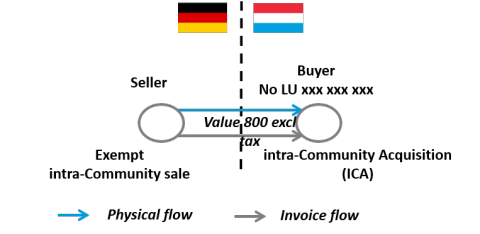

For example: a Luxembourg company orders goods from a German supplier and provides its supplier with its Luxembourg VAT number. The goods are delivered in Luxembourg.

It receives an invoice without VAT from its supplier. It must declare an intra-Community acquisition taxable in Luxembourg. It immediately claims the deduction of the VAT thus paid in the same return.

| VAT DECLARATION OF THE BUYER | |

|---|---|

|

VAT due |

AIC: 136 EUR (800*17%) TOTAL: 136 EUR |

|

Deductible VAT |

ICA: 136 EUR TOTAL: 136 EUR |

| Balance | To pay: 0 EUR

|

"Triangular" intra-Community transactions

Certain goods are subject to successive sales involving one single transport. In this case, only one supply can benefit from the intra-Community exemption. The other sales are national transactions.

A simplification measure applies for so-called "triangular" transactions. This simplification measure allows to issue two invoices without VAT for chain transactions involving a purchaser/intermediate reseller with a single physical transport of the goods. The simplification measure can only apply to successive sales of goods involving three operators identified for VAT in three different Member States, with direct transport of the goods from the initial supplier to the final purchaser.

For example: a Luxembourg company (B) receives an order from a German customer (C), which provides it with its German VAT number. The Luxembourg company (B) orders goods from a French supplier (A) and asks the supplier to deliver the goods directly to its German customer (C).

- the sale by the French supplier (A) is an intra-community supply of goods exempt in France

- the purchase made by the Luxembourg company (B) is not subject to VAT in application of the triangular simplification measure

- the sale by the Luxembourg company (B) is an exempt subsequent supply of goods in application of the triangular simplification measure

- the German purchaser (C) declares an intra-Community acquisition in Germany.

The following procedures and declarations must be followed for implementation of the triangular simplification measure:

- the transport is organized by the first (A) or by the second (B) operator or by a third-party acting on their behalf

- the second operator (B) declares, in its VAT return, the acquisition and the subsequent supply of goods in specific lines for triangular transactions

- the second operator (B) declares its triangular sale in a recapitulative statement and makes specific mention of such in its sale invoice

- the final acquirer (C) declares an intra-Community acquisition in its VAT return as the final tax debtor.

Intra-Community sale to a "non-taxable" person

An intra-Community sale to a "non-taxable" person is always subject to VAT.

If the customer takes possession of the goods, the supplier is making a national supply of goods and must invoice the VAT of the Member State in which the goods are located at the time of the supply.

If the seller organizes the transport, the distance sales procedure applies:

Since 1 July 2021, the seller must invoice his customer for the VAT of the country of destination of the goods. The seller can declare and pay the VAT due in the other Member States with the Luxembourg authorities, using the OSS ("One Stop Shop") system.

By exception:

- the seller established in the EU whose global sales and provision of electronic services to persons in the EU does not exceed EUR 10,000 can invoice for the VAT of the country of departure of transport

- the delivery of a new vehicle (fewer than 6,000 km or less than 6 months) is taxable in the country in which the vehicle will be registered. The buyer must pay the VAT in accordance with the procedure specified by the country in question. In Luxembourg, the VAT must be paid to the Customs and Excise Administration prior to registration

- the sale of second-hand goods, art objects, collectibles and antiques that can benefit from the special profit margin scheme is still taxable in the country of departure of the transport

- the sale of goods delivered after installation or assembly is taxable in the country in which the installation or assembly is performed

If the seller opts for the IOSS to declare sales to private individuals, he must:

- submit a quarterly VAT declaration electronically using the OSS portal

- make a quarterly payment of the corresponding VAT with the Member State of its OSS identification

- keep detailed records of all sales declared through the OSS, and keep such records for ten years

* From a VAT point of view, one still speaks of the European community and not of the European Union. For reasons of consistency, we will use the term "Union" in this portal.

INTRASTAT declaration

Movements of goods between Member States must be declared, for statistical purposes, by filing Intrastat declarations.