Value-added tax (VAT) covers all stages of production and distribution of goods carried out within the territory of Luxembourg.

National transactions subject to Luxembourg VAT are the following:

- sales of goods delivered in Luxembourg, in which goods are located at the time when the dispatch or transport starts

- supplies of goods with installation or assembly in Luxembourg

- sales of goods that are imported and delivered in Luxembourg by the supplier

- distance sales of goods delivered to a non-taxable person in Luxembourg, when the supplier has exceeded the threshold of distance sales to Luxembourg (EUR 100,000). From 1 July 2021, all distance sales of goods delivered to a non-professional customer in Luxembourg will be taxable in Luxembourg from the 1st Euro.

The following transactions are also subject to Luxembourg VAT:

- imports of goods declared to customs in Luxembourg

- intra-community acquisitions (ICA) of goods delivered to Luxembourg.

An economic operator that carries out one of these transactions must comply with Luxembourg VAT laws and regulations. He must invoice and/or declare the VAT due in Luxembourg regardless of the country in which he is established.

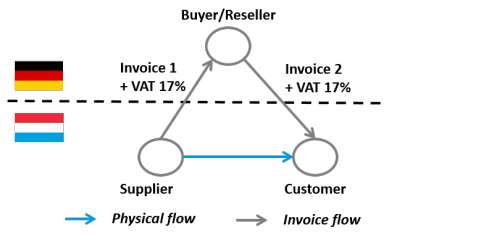

Examples of national transactions and their VAT consequences (example at 17% VAT): A German buyer orders computers from a Luxembourg supplier.

The buyer has them delivered directly to his Luxembourg customer by his supplier.

The two sales are national transactions subject to Luxembourg VAT and are taxable in Luxembourg at the normal rate.

Invoice 1: sale located in Luxembourg, since there is no exit of goods from the national territory

Invoice 2: sale located in Luxembourg: place where the goods are located at the time of the sale. The German company owes the VAT on sale 2. It must register for Luxembourg VAT and declare the transactions that it carried out in Luxembourg: invoice 1, tax deductible / invoice 2: sale and VAT payable.

VAT rates applicable in Luxembourg

The VAT rate to invoice depends on the nature of the goods concerned.

Standard 17% rate

The standard rate of 17% applies to all goods and services not subject to one of the reduced rates below.

Intermediate 14% rate

The intermediate rate of 14% applies to the following goods:

- wine from fresh grapes at 13% alcohol or less, except for fortified wines, sparkling wines and so-called liqueur wines

- solid mineral fuels, mineral oils and wood intended to be used as fuel, except for wood used for heating that is subject to a reduced rate

- preparations for detergent and cleaning preparations

- printed advertising materials, commercial catalogs and similar items; tourism promotion publications.

Reduced 8% rate

The reduced rate of 8% normally applies to the following goods:

- liquefied or gaseous gas, used for heating, lighting and motor fuel

- live plants and other floricultural products

- intra-Community supply and acquisition of works of art, by their creator or his successors in title

- importation of works of art, collectors' items and antiques.

Super reduced 3% rate

The super reduced rate of 3% applies to the following goods:

- food products, excluding alcoholic beverages

- feed

- therapeutic articles and medical devices for disabled persons

- agricultural entries, excluding products falling under heading no. 38.08 of the combined customs nomenclature

- books, newspapers and periodicals except for advertising material and pornographic books, newspapers and publications

- shoes and clothing for children less than 14 years of age

- pharmaceutical products such as:

- pharmaceutical specialties, ready-made medecines and medecines for human usage

- veterinary medicinal products

- pharmaceutical preparations

- products used for contraception.

- products used for feminine hygiene protection

Supply of manufactured tobaccos

Supply of manufactured tobaccos are subject to a special VAT scheme. This concerns the supply of cigarettes, cigars and cigarillos, smoking tobaccos, snuff or chewing tobacco. This special scheme is specified by a Grand-Ducal regulation based on the VAT law.

It is however possible to use a VAT suspensive arrangement, that suspends the application of the special scheme. Manufactured tobaccos placed in a tax warehouse are considered to be in the VAT warehouse suspensive arrangement. Upon removal from the VAT suspensive arrangement, the VAT due on manufactured tobaccos is paid by the operator responsible for the warehouse to the Customs and Excise Administration.